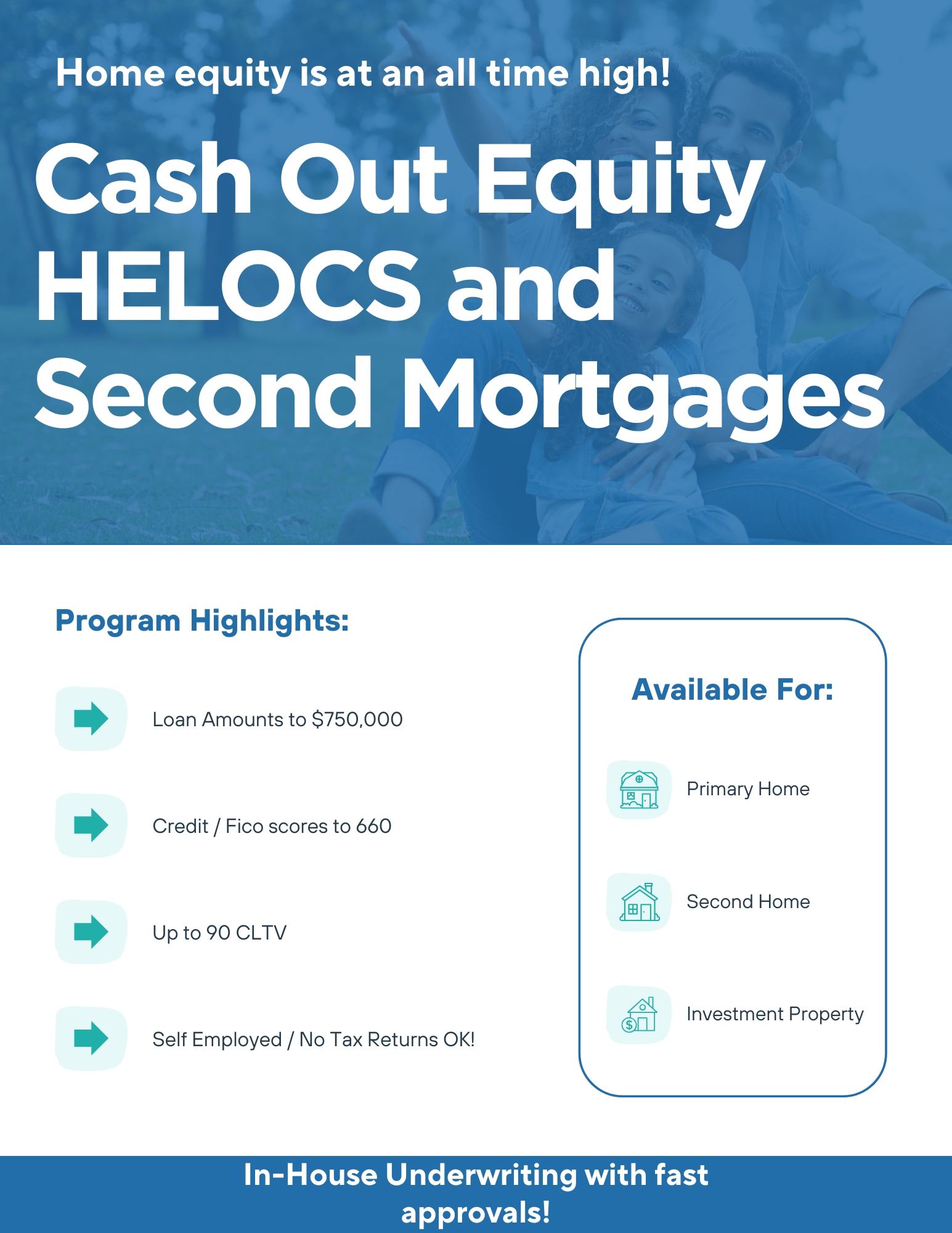

Both a Home Equity Line of Credit (HELOC) and a fixed second mortgage have their own unique benefits. Here's a comparison to help you understand which might be better for your needs:

HELOC (Home Equity Line of Credit)

- Flexibility: A HELOC works like a credit card. You can borrow as much as you need, up to your credit limit, and repay it over time. This makes it ideal for ongoing expenses or projects where the total cost is uncertain1.

- Interest Rates: HELOCs typically have variable interest rates, which can start lower than fixed rates. However, they can fluctuate based on market conditions2.

- Payment Structure: During the draw period, you usually only need to make interest payments. This can make initial payments lower compared to a fixed second mortgage2.

- Lower Closing Costs: HELOCs often have lower closing costs compared to fixed second mortgages2.

Fixed Second Mortgage

- Predictability: With a fixed second mortgage, you receive a lump sum upfront and repay it with fixed monthly payments over a set term. This predictability can be beneficial for budgeting3.

- Fixed Interest Rates: The interest rate is fixed for the life of the loan, providing stability and protection against rising interest rates3.

- Lump Sum: If you need a large amount of money for a specific purpose (like a major home renovation), a fixed second mortgage can be more suitable since you get all the funds at once3.

Which to Choose?

- HELOC: Best if you need flexibility, have ongoing expenses, or want to take advantage of potentially lower initial interest rates.

- Fixed Second Mortgage: Best if you prefer predictable payments, need a large lump sum, or want to lock in a fixed interest rate.

Ultimately, the right choice depends on your financial situation and goals. If you have any specific needs or questions, feel free to ask! Contact me today to see what is the best option for you